The New Trade Map - China’s Export Pivot to the Global South. Friday’s Edition

The trade map America isn’t on - Series 14 #5

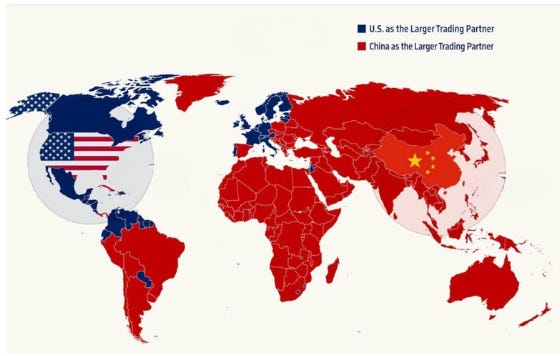

The United States is not included in RCEP, the CPTPP, or EU-Mercosur, and while this is a significant disadvantage for American companies, something bigger looms. China is a member of only one, the RCEP, but trades heavily with members of all three trade blocs. The Trump-Republican administration has pushed all of these countries away from the U.S. and…